Second homes have been the unlikely recipient of massive appreciation since the pandemic.

Vacation hot spot, Florida, experienced 56% growth in home prices between November 2019 and November 2023, an increase of $146,000 on average, says Redfin.

Vacation property owners are now wondering how to leverage this newfound equity.

Fortunately, conventional lending allows cash-out refinances on second homes, and the process is similar to a standard refinance.

Here’s how to tap your secondary residence equity for cash.

See if you can turn second home equity into cash. Start here.

- 1. Prove second home status versus an investment property

- 2. Determine how much cash out you can get (and if it’s worth it)

- 3. Make sure you’re eligible

- 4. Get a second opinion on value

- 5. Find a lender

- 6. Get the best rate/fee structure

- 7. Submit documentation and close the loan

- Is your loan a “cash out,” “limited cash-out,” or “no cash-out”?

- Uses for vacation home cash-out refinance funds

- FAQ

- Mortgage rates could drop, making a second home cash-out refinance worth it

1. Prove second home status versus an investment property

First, you want to make sure the lender can accept your property as a second home and not an investment property.

While mortgage rates are about the same for each property, they require different guidelines.

That being said, you are allowed to show some short-term rental income from Airbnb and other rental services. You can’t use this income to qualify.

Here’s how you verify its second home status

- You occupy the home some portion of the year (typically at least 10% of the number of days it’s rented)

- It’s a one-unit dwelling (no 2-4 unit properties).

- Suitable to occupy year-round.

- No other entity has control of the property. You have sole control.

- There’s no management company or booking agency controlling occupancy.

Start your second home cash-out refinance.

2. Determine how much cash out you can get (and if it’s worth it)

Lenders limit your loan-to-value ratio (LTV) based on Fannie Mae and Freddie Mac standards.

| Loan type | Second home | Investment property |

| Cash-out refi | 75% LTV | 75% |

| No-cash-out refi | 90% LTV | 85%* |

*Available from Freddie Mac lenders on 1-unit properties only. Fannie Mae limit is 75% LTV

Make sure you can get enough cash to justify the closing costs. For instance, don’t spend $7,500 in closing costs to get $10,000 cash back unless you have another reason to refinance.

For instance:

Scenario 1: Likely worth a cash-out refi

| Home value | $350,000 |

| Existing loan | $150,000 |

| Max loan | $262,500 |

| Closing costs | $7,500 |

| Cash to you | $105,000 |

Scenario 2: Likely NOT worth a cash-out refi

| Home value | $350,000 |

| Existing loan | $225,000 |

| Max loan | $262,500 |

| Closing costs | $7,500 |

| Cash to you | $30,000 |

Spending $7,500 in closing costs to get $30,000 is probably not worth it. Try opening up a home equity line of credit (HELOC) on the second home or your primary residence, or taking a personal loan.

3. Make sure you’re eligible

Following are other guidelines.

Credit score: 620 minimum. But you’ll get the best rates and higher chances of approval with a 700+ score.

Cash reserves: You’ll need cash reserves based on properties owned, not including the subject property or primary residence. “Reserves” are simply funds in checking, savings, and investment accounts. Lenders need to see that you can pay for your properties if you lose your source of income. Cash received with the refinance does not count toward reserve requirements.

- 2% of unpaid balances if you own 1-4 financed properties

- 4% of unpaid balances if you own 5-6 financed properties

- 6% of unpaid balances if you own 7-10 financed properties

Debt-to-income (DTI) ratio: All your debts – primary residence, second home payment, auto loans, etc. – should be no more than about 43% of your gross income. Your DTI can be difficult to figure out on your own, so apply with a lender if you’re unsure of your DTI.

Start your refinance approval process here.

4. Get a second opinion on value

Home prices are cooling, and may even be dropping in some areas.

Before you spend $500+ on an appraisal, ask a lender or Realtor for a price opinion.

If your appraised value comes in low, you may not have access to the cash you expected. But, you’ll still be on the hook for the appraisal cost.

5. Find a lender

Explore many different types of lenders to find the best rates and terms.

Try the bank where you have a checking account, local credit unions, mortgage companies, national banks, and mortgage brokers.

Get started with a second home cash-out lender here.

6. Get the best rate/fee structure

Because your loan has two non-standard loan features (cash out and second home) you might find that some lenders either can’t do it at all, or charge sky-high rates and fees.

You may have to pay points with cash or roll it into the new loan.

Further complicating things, Fannie Mae increased discount point requirements for second homes. Now, second home rates are similar to those of investment properties.

Here are points required for a second home cash-out refinance at a 700 credit score.

| Loan Feature | Points |

|---|---|

| 700 FICO score / 75% LTV | 1.0 |

| Second home | 2.125 |

| Cash-out | 1.0 |

| Total | 4.125 |

On a $300,000 loan 4.125 points is $12,375 in additional closing costs. Most people choose to take a higher rate in lieu of the fees; these points would raise your rate by about 1.5-2.5%.

Unfortunately, your rate might jump substantially compared to your existing rate.

Make sure you’re getting enough benefit before taking a higher rate.

7. Submit documentation and close the loan

Apply with your lender of choice. Your loan officer will request your documentation, order the appraisal, and submit the file to underwriting.

You’ll get another set of requests, called conditions. Supply these as quickly as possible.

Soon, your file will receive a “clear to close,” meaning it’s ready for final paperwork. Sign final docs at the escrow company.

A few days later, the loan will fund. That same day, you should see the cash in your account. It’s a great feeling to receive real dollars based on the theoretical value of the home.

Is your loan a “cash out,” “limited cash-out,” or “no cash-out”?

As shown above, you’re being charged an extra 1.0 in points to do a cash-out loan. Make sure you can’t classify the loan as “no cash-out.”

“No cash-out” and “limited cash-out” are the same thing. They just mean you are not taking significant extra cash beyond what it takes to close the loan.

Here are items the extra loan amount you CAN include in the new loan, according to Fannie Mae:

- Closing costs

- Points

- Prepaid items like taxes and insurance

- Primary mortgage balance

- Subordinate financing/second mortgage balances

- The lower of $2,000 or 2% of the new loan amount

Say you need $7,000 in cash. To close the loan, the lender requires you to prepay a few items:

- Eight months at $400 per month

- $500 in insurance premiums.

- One month interest because you close on the first of the month ($1,500).

After all that, you get a loan amount that is roughly $2,000 above the amount to cover all this. Here’s the cash you can receive.

- At closing: $2,000

- A few weeks after closing: $3,700 (prepaid taxes and insurance sent back to you from your current mortgage servicer)

- “Skipping” a payment because you closed on the 1st: $2,000

Here, you financed roughly $7,000 into the new loan, even though it’s still considered a “no cash-out” refinance. If you don’t need a lot of cash, save some money and/or get a lower rate by classifying the loan as no cash-out.

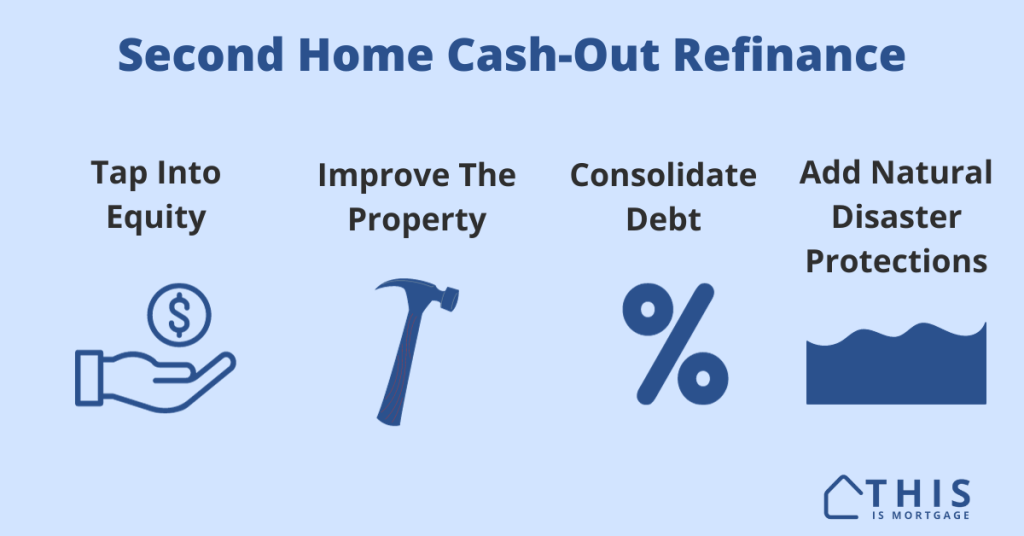

Uses for vacation home cash-out refinance funds

Generally, getting cash out is a good idea if you’re improving the home and increasing its value or longevity.

- Remodel the interior

- Update the roof, siding, windows, and other large maintenance items

- Add natural disaster protections

- Add a bedroom or bathroom to increase short-term rental profit

- Add an outdoor living space

- Consolidate a high-interest second mortgage

FAQ

Yes, lenders allow you to take cash out on a second home refinance up to 75% of the home’s current value. The process is the same as for a standard refinance. The only difference is that you increase your loan amount to get extra cash back at closing.

You will need a minimum 620 score, although 700+ is preferred for better rates and higher chances of approval.

Your loan balance will rise, raising your monthly payment. Also, it’s quite likely that your interest rate will increase due to Fannie Mae second home cost increases rolled out in early 2022. Additionally, your loan will start over at 30 years unless you refinance into a shorter-term loan.

Mortgage rates could drop, making a second home cash-out refinance worth it

Rates are high in early 2024, but could drop as the year goes on.

It could be a great time to tap into the equity in your vacation home.

Start your refinance approval process.