Contrary to common belief, many self-employed individuals are eligible for a mortgage.

Yes, getting approved takes creativity and harder work, but most don’t mind that part: it’s their daily lives as business owners.

Luckily, FHA loans are one of the most lenient programs for self-employed applicants.

See if you’re eligible for an FHA loan.

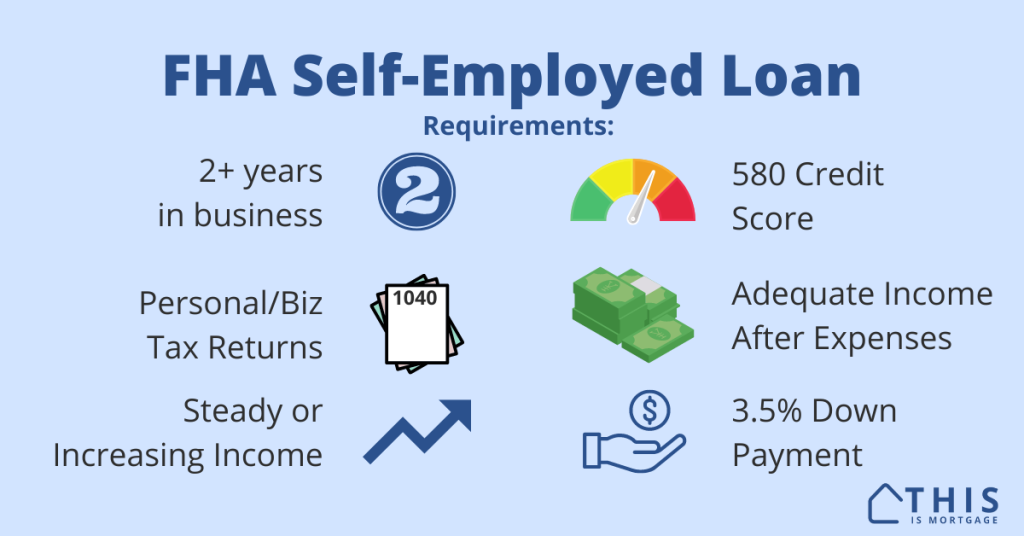

FHA loan self-employed requirements

- 2+ years of self-employment (1+ year acceptable in some cases)

- 2 years personal tax returns

- 2 years business tax returns

- Year-to-date profit and loss statement and balance sheet could be required

- Adequate net taxable income after expenses

- Proof of two years in business such as a business license or CPA letter

- Steady or increasing income over the past two years preferred; declining income of 20% or more is usually not acceptable

There are exceptions to some of the requirements above, so see below to learn more.

General FHA loan requirements for all borrowers:

- 3.5% down payment

- 580 credit score (500 with 10% down)

- Max 56.9% debt-to-income ratio

- Adequate funds, gift money, and/or down payment assistance for the down payment and closing costs

- Find an adequate home such as a single-family residence, multifamily, or mixed-use building

Check your FHA eligibility as a self-employed individual.

How the lender calculates income

Self-employed income is less defined than with a W2 job. It’s often much harder to determine how much you make from a lender’s perspective.

Here are rules of thumb:

Sole proprietor: Schedule C, Line 31. Add back in Depreciation, Depletion, Amortization/Casualty Loss and Business Use of Home.

Partnership/S-Corp: Schedule 1065 or 1120s. Ordinary Business Income/Loss + Other Net Rental Income + Net Rental Real Estate + Guaranteed Payments. Add back in Depreciation + Depletion + Amortization. Subtract Mortgage/Notes Payable in less than 1year. Multiply by percentage of ownership and add W2 income from that business.

C-Corp: Form 1120. Net Profit/Loss (Line 31) – Total Tax (Line 28). Add back in Depreciation + Depletion + Amortization. Subtract Mortgage/Notes Payable. Multiply by percentage of ownership and add W2 income from that business.

Now take income from the last two years and divide by 24. This is your monthly income.

For example:

20XX: $110,000

20XX: $120,000

Total: $230,000 / 24 = $9,583/mo

However, if your most recent year was lower, the lender may use this figure divided by 12. The lender may deny a loan if income dropped more than 20% in the most recent tax return year.

There are other caveats and rules. The best way to get a self-employed income analysis is to submit your full application and documents to a lender for a pre-approval.

Getting approved with 1 year of self-employment

FHA allows self employment for some applicants with just one year of filed tax returns. To be eligible you must:

- Have been employed in the same line of work before transitioning to self-employed

- You have a strong two-year history in the previous W2 role

For example, you were a software engineer for two years with no gaps from 2021 to 2022. In January 2023, you became a 1099 contractor or started your own software engineering consultancy. You may be eligible for FHA as soon as you file taxes for 2023.

See if your self-employed history qualifies you for FHA.

When you don’t need business tax returns

The lender may waive the requirement for two years of business tax returns when:

- Personal tax returns show increasing self-employment income over the past two years

- You are not using business accounts for the down payment or closing costs

- You are buying a home or getting a no-cash-out refinance. Cash-out refinances require business returns

Supplying a P&L

FHA lenders require a profit and loss statement when you apply after the first quarter of the year. Everyone besides sole proprietors need a balance sheet as well.

The lender may ask for a quarterly tax return or audited P&L if the current year income appears to be in decline.

What about side gigs?

Many people have W2 jobs and have a self-employed business on the side. You would have to show a history of working both jobs simultaneously to count both income sources.

For others, a self-employed business is their primary income, but they have a part-time job as well. This, too, would require a two-year history of simultaneous work.

There are no exceptions to the two-year rule for two income sources.

The lender needs to know the borrower can and will maintain both jobs after the loan closes.

What if I’m only part owner in a business?

Anyone with 25% or more ownership in a business is considered self-employed and must submit personal and business tax returns.

If you are 10% owner in a business, for example, you do not have to supply tax returns unless you want to use that income to qualify.

See your self-employed FHA loan eligibility status.

What if my side business shows a loss?

Some small side businesses like an Etsy shop or small consultancy show a loss for the year. Some even run an unprofitable business for tax savings.

FHA requires the lender to count side business losses against income. So if you make $100,000 per year but have a $20,000 side business loss, your qualifying income is $80,000 per year.

The lender will find out about your side business (even if you don’t submit tax returns). It will request tax transcripts directly from the IRS before approving the loan.

If the loss will keep you from qualifying, consider terminating your business and license. Supply any other documentation for proof of closure. Then write a letter of explanation. Run the scenario by an underwriter first, though. There’s no guarantee they will believe you truly ceased operations.

Some conventional loans from Fannie Mae do not require the lender to count side business losses against the borrower. This may be another option if you have a business that loses money.

Using business funds toward down payment or closing costs

You are allowed to use funds from a business bank account toward funds to close. This will trigger the requirement to show business tax returns.

Additionally, the lender may require a CPA letter stating that removing funds won’t jeopardize the business. Expect extra scrutiny if you have a capital-intensive business that requires you to outlay large amounts of cash for payroll, inventory, or other items.

Business debt

The lender is not required to count business debt showing up on your credit report into your DTI. In effect, this would be “hitting you with” the debt twice if the debt payments are already removed from your business income.

Supply proof that the business pays the debt via receipts or bank statements.

Closing in the name of a business

It is not possible to close in the name of an LLC or other business entity with an FHA loan. You must purchase the home as an individual. You would have to find a business-purpose loan, DSCR, or other non-QM product to close in the name of a business.

Transferring ownership to a business after closing is possible with FHA, but tread carefully. You must get approval from HUD to do so and there’s no guarantee they will grant it. The business type must be an LLC (no Partnerships, S-Corps or C-Corps). Get legal counsel prior to transferring ownership. It could trigger a due-on-sale clause, meaning you would have to pay off or refinance the loan to another loan type immediately.

You can get a mortgage as a self-employed borrower

While it’s harder to prove than W2 income, self-employed earnings are earnings just the same.

The biggest issue most people run into is lack of taxable income. If you’re looking to get a mortgage in the next few years, ease up on your write-offs.

With some planning, you can show enough income to qualify.

Start your self-employed FHA loan.