Shopping for a better mortgage rate is not nearly as exciting as searching for the best deal on a car or hotel room.

Yet, more than one-third of homebuyers requested only one quote during the mortgage process, says a study by mortgage giant Fannie Mae.

Meanwhile, Expedia reports that vacationers review 38 websites before booking a hotel room.

Another mortgage agency, Freddie Mac, conducts a weekly survey of mortgage rates offered by various lenders. It found that rates can vary as much as 0.6% from one lender to the next.

The difference between a 0.6% better mortgage rate and saving $50 on a hotel room is astounding, yet many consumers still refuse to shop.

(If you’re wondering, you can save $71,624 by shopping for a mortgage, assuming Freddie Mac’s 0.6% rate difference over 30 years on a $500,000 loan.)

Here’s are five tips to help you resist the urge to settle for your first mortgage quote.

Start shopping for rates here.

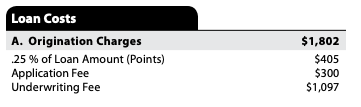

1. Review Only Certain Closing Costs

Many consumers don’t shop for mortgages based on closing costs because it seems entirely too complex.

There are dozens of line items in the Loan Estimate, or “LE” – the document that the lender is required to give you. It’s your official quote.

Most consumers don’t know how much a fee should be, and that’s okay.

To make things simple, only review costs on Page 2, Section A: Origination Charges. These are lender charges. Loan origination fee, discount points, application fees, and underwriting fees will appear here.

Compare Section A charges from one lender with those from two or three others.

Don’t look at costs in lines B and C. These are third-party charges for things like title, escrow, appraisal, and credit report. They have little to do with the lender. You’ll probably pay similar fees no matter which lender you choose.

Yes, you can shop for some of these items, but the bulk of savings will come from negotiating down the lender charges, or choosing a lender with lower fees in Section A.

Connect with a lender to get a closing cost estimate.

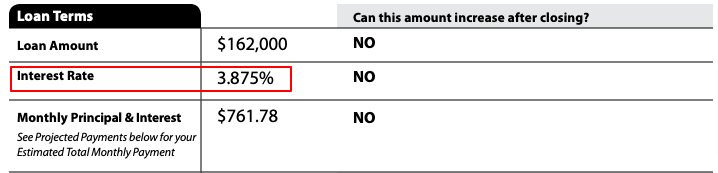

2. The Mortgage Rate Doesn’t Tell The Whole Story

A low quoted rate may not be a good deal.

Sure, a lender can beat another lender by 1% in rate, but might charge you $20,000 in points to do so.

That’s why you want to review both the mortgage rate on Page 1 of the Loan Estimate together with Section A charges on Page 2.

For instance, Lender X gives you a 6.5% rate with $3,000 in Section A Origination Charges. You spend 10 minutes calling or getting an online quote from Lender Y, which offers 6.5% with $1,000 in Section A.

Ask Lender X to match Lender Y’s offer. Or, just go with Lender Y. You just saved $2,000 for 10 minutes of work.

You can potentially make more in a few minutes than you do in an entire week at your day job.

But don’t stop there. Call three or four other lenders to see if you can reduce your rate and fees. You’d be surprised at how much rates and fees vary depending on each lender’s motivation to earn your business.

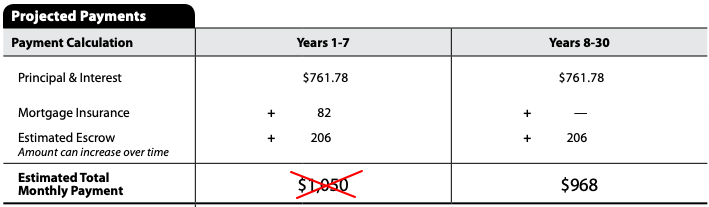

3. Don’t Shop For Monthly Payment

According to Fannie Mae’s research, the monthly payment was the second most shopped-for item behind interest rate.

The thing about monthly payment is that it can be skewed by the loan officer’s estimates of property taxes and insurance.

When looking at the Loan Estimate, review “Monthly Principal & Interest” rather than “Estimated Total Monthly Payment.”

In the screenshot above, imagine if Lender X and Lender Y quote both you a $761.78 principal and interest payment. But Lender X unrealistically estimates $106 per month for “Escrow” (taxes and insurance) instead of $206.

Lender X looks like the better deal with a $950 monthly payment versus Lender Y’s more realistic $1,050. Until you realize that no lender has any control over your future property taxes and homeowners insurance.

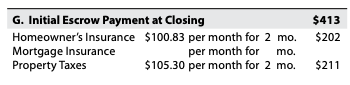

4. Closing Costs Are Estimates. Treat Them As Such

Don’t move on to a different lender because estimated closing costs or cash to close look higher at one lender than another.

Your final cash-to-close numbers largely come from items outside the lender’s control, like the number of months of taxes collected.

As with monthly tax estimates above, a less reputable loan officer can underestimate your tax numbers. This makes his offer appear better.

For instance, estimating two months of collected taxes instead of six makes a $1,600 difference in cash to close if property taxes are $400 per month.

A new homebuyer may go with the loan officer who “offered” to collect only two months. But that’s not up to the loan officer. The amount collected will be the same no matter which lender you go with. It depends on when and how often during the year your county collects taxes.

In short, completely disregard estimates for prepaid taxes and insurance, at least when it comes to comparing lenders.

5. Embrace Hard Conversations

This tip sounds cold, but you should go about shopping for a mortgage to get the best rate, not to make a friend.

Loan officers’ secret weapon is to make you like them so that you won’t shop around. They are trained to build rapport with you immediately.

This is perhaps why so many homebuyers settle for their first rate quote. According to the Fannie Mae study, 39% of buyers only got one quote because they were “comfortable with the lender they received the quote from.”

Have hard conversations. Get quotes from other lenders and make your favorite loan officer match their deal. If they can’t, move on.

In five or ten years, you probably won’t be in contact with your loan officer. But you might still be paying hundreds more per month because you got too friendly with your loan officer.

No one said mortgage rate shopping was easy. And questioning your loan officer could be the hardest part. But in the end, you’ll be glad you took the extra time and effort to get a better deal.

Shop for rates with top lenders. Start here.

Images in this post: Consumer Finance Protection Bureau