When you refinance one FHA loan to another FHA loan, you may be entitled to a partial refund of the upfront mortgage insurance premium (upfront MIP).

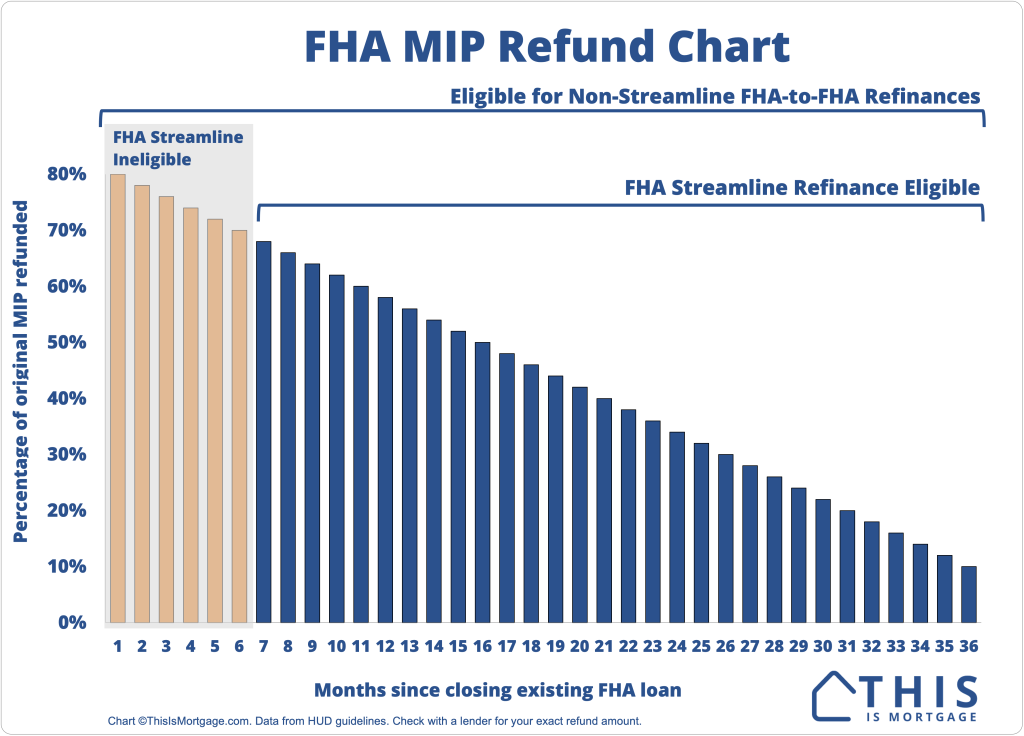

How much you get back and how it can be used are important details, but to begin, let’s take a look at these FHA MIP refund charts. This table shows the percentage of your expected refund and how that converts to real dollars on a $200k, $300k, and $400k original FHA loan amount.

See how much you can save with an FHA refinance.

| Months after closing | MIP refund | $200k orig. loan | $300k orig. loan | $400k orig. loan |

| 1 | 80% | $2,800 | $4,200 | $5,600 |

| 2 | 78% | $2,730 | $4,095 | $5,460 |

| 3 | 76% | $2,660 | $3,990 | $5,320 |

| 4 | 74% | $2,590 | $3,885 | $5,180 |

| 5 | 72% | $2,520 | $3,780 | $5,040 |

| 6 | 70% | $2,450 | $3,675 | $4,900 |

| 7 | 68% | $2,380 | $3,570 | $4,760 |

| 8 | 66% | $2,310 | $3,465 | $4,620 |

| 9 | 64% | $2,240 | $3,360 | $4,480 |

| 10 | 62% | $2,170 | $3,255 | $4,340 |

| 11 | 60% | $2,100 | $3,150 | $4,200 |

| 12 | 58% | $2,030 | $3,045 | $4,060 |

| 13 | 56% | $1,960 | $2,940 | $3,920 |

| 14 | 54% | $1,890 | $2,835 | $3,780 |

| 15 | 52% | $1,820 | $2,730 | $3,640 |

| 16 | 50% | $1,750 | $2,625 | $3,500 |

| 17 | 48% | $1,680 | $2,520 | $3,360 |

| 18 | 46% | $1,610 | $2,415 | $3,220 |

| 19 | 44% | $1,540 | $2,310 | $3,080 |

| 20 | 42% | $1,470 | $2,205 | $2,940 |

| 21 | 40% | $1,400 | $2,100 | $2,800 |

| 22 | 38% | $1,330 | $1,995 | $2,660 |

| 23 | 36% | $1,260 | $1,890 | $2,520 |

| 24 | 34% | $1,190 | $1,785 | $2,380 |

| 25 | 32% | $1,120 | $1,680 | $2,240 |

| 26 | 30% | $1,050 | $1,575 | $2,100 |

| 27 | 28% | $980 | $1,470 | $1,960 |

| 28 | 26% | $910 | $1,365 | $1,820 |

| 29 | 24% | $840 | $1,260 | $1,680 |

| 30 | 22% | $770 | $1,155 | $1,540 |

| 31 | 20% | $700 | $1,050 | $1,400 |

| 32 | 18% | $630 | $945 | $1,260 |

| 33 | 16% | $560 | $840 | $1,120 |

| 34 | 14% | $490 | $735 | $980 |

| 35 | 12% | $420 | $630 | $840 |

| 36 | 10% | $350 | $525 | $700 |

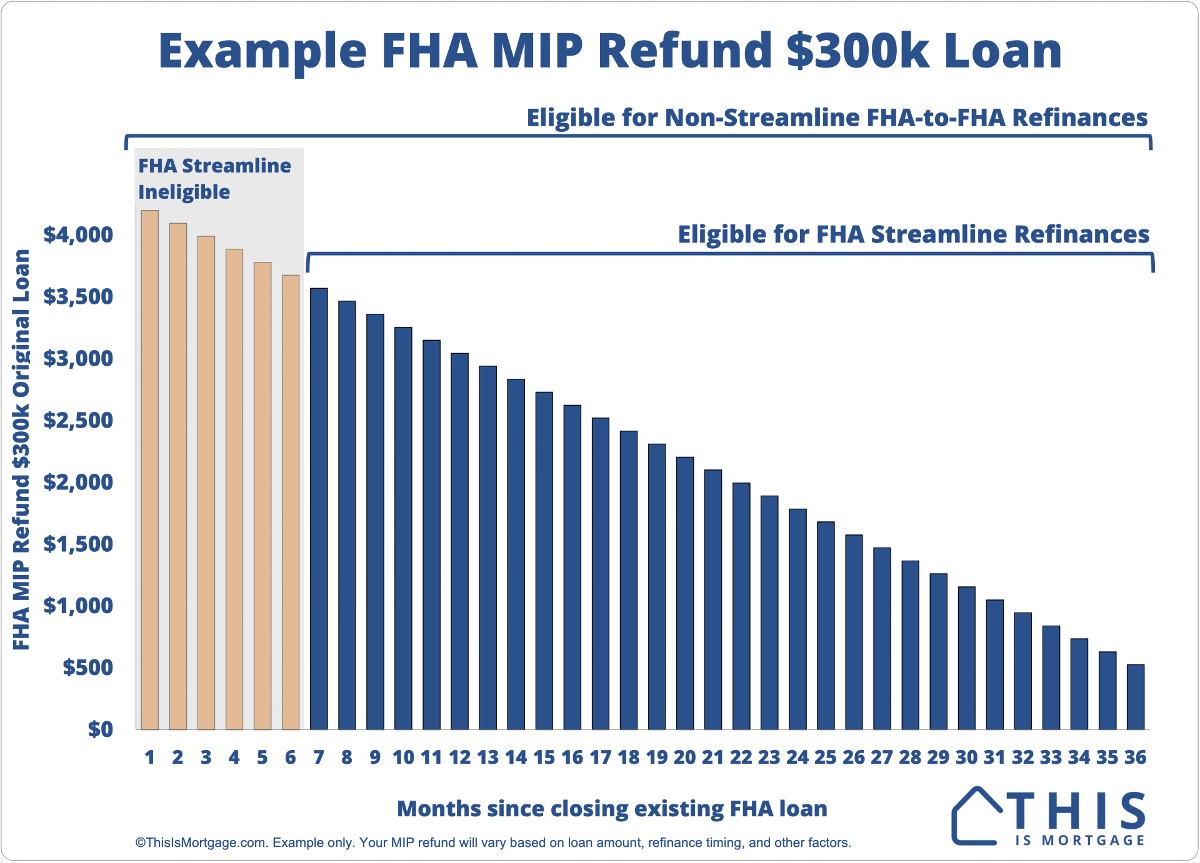

Refund when refinancing a $300k original FHA loan amount

To put it visually, here is a chart showing the potential refund on a $300,000 original FHA loan amount.

You may be eligible for a very large MIP refund or a small one depending on your original loan amount and how long it’s been since you closed the loan.

Connect with a lender to check your MIP refund amount.

How to get your refund

You have to meet a few conditions to receive an FHA MIP refund:

- You are refinancing an FHA loan to another FHA loan

- Your last FHA loan closed less than 3 years ago

For most things, a “refund” implies cash-in-hand. Unfortunately, FHA does not pay cash refunds for MIP.

Rather, the refund is applied to the upfront mortgage insurance premium on your new refinance loan.

For example:

| Upfront MIP due on new loan | $5,000 |

| MIP refund | -$3,000 |

| Reduced upfront MIP on new loan | $2,000 |

Instead of paying over $5,000 for upfront MIP (essentially paying that upfront fee twice within a couple years), it’s reduced to $2,000.

Here’s how to calculate your refund and new upfront MIP

- Original loan amount X 1.75%

- Times the refund percentage from the above chart

- Equals the refund amount

Now remember that refund amount for the next step.

- New loan amount X 1.75%

- Minus the refund amount

- Equals new upfront MIP

For example:

- Your original FHA loan was $300,000 and upfront MIP was $5,250 ($300k X 1.75%).

- It’s been 12 months since closing. You are eligible for a 58% refund.

- The refund amount is $3,045

- New loan amount is $295,000; new upfront MIP is $5,162 ($295k X 1.75%)

- Minus $3,045 refund

- Upfront MIP on new loan: $2,117

Most lenders will automatically apply your MIP refund to the refinance. If they don’t, be sure to bring it to their attention.

FHA refinance waiting periods

The most popular type of FHA refinance is the FHA Streamline. It lets you lower your rate to current market levels with no appraisal, income documentation, or even a credit report.

But you must wait 210 days from your previous loan closing to complete the new loan. So getting a refund of more than 68% is impossible with the Streamline program.

However, there is no waiting period for other FHA refinance types, such as:

- FHA Cash Out: Take equity out of your home

- FHA Simple Refinance: Replace your existing FHA loan with a new one and wrap in closing costs. Requires an appraisal and full documentation.

For example, you purchase a home with an FHA loan. Two months later, rates drop. You could get a new FHA loan and an MIP refund of 78% with a new full-doc FHA refinance.

It could be worth waiting six months for the FHA streamline option, though. With it, you’ll save around $700 on appraisal charges and skip the hassle of collecting paystubs, W2s, and other documentation.

Do you get a refund when you refinance into another loan type?

Unfortunately, FHA offers refunds on FHA-to-FHA refinances only.

That doesn’t mean refinancing into another type of loan is a bad idea.

Conventional mortgage insurance is cancelable in the future, whereas FHA mortgage insurance is permanent. Also, you can remove FHA mortgage insurance with a conventional loan if you have enough equity in the home.

Sometimes it’s worth losing your upfront FHA MIP refund to save hundreds per month in mortgage insurance costs.

Start your FHA refinance and get your maximum MIP refund

Your refund amount goes down by 2% for each month you wait to refinance. That’s why it’s often worth it to refi sooner rather than later, assuming an FHA-to-FHA refinance.

Get started on your FHA refinance, which can be much quicker and less expensive than your original FHA loan.