Buying a duplex, triplex, or fourplex, and now a single-family with an ADU is one of the smartest things you can do in real estate.

You become a homeowner and a landlord with one transaction.

But not every buyer knows about an FHA rule that could make it easier to buy a multifamily property than a single-family (1-unit) home.

FHA rental income guidelines in 2024 point out the ability to use future rents on the subject property to qualify.

Speak to a lender to see if you can become a multifamily homeowner.

In this article:

- How to qualify more easily using future rents

- Prove future income

- Maximizing future rental income

- The appraiser’s rental income reports

- Rental income from another property

- FHA self-sufficiency test

- Lender says you can’t use future rent

- How to apply

How to qualify more easily using future rents

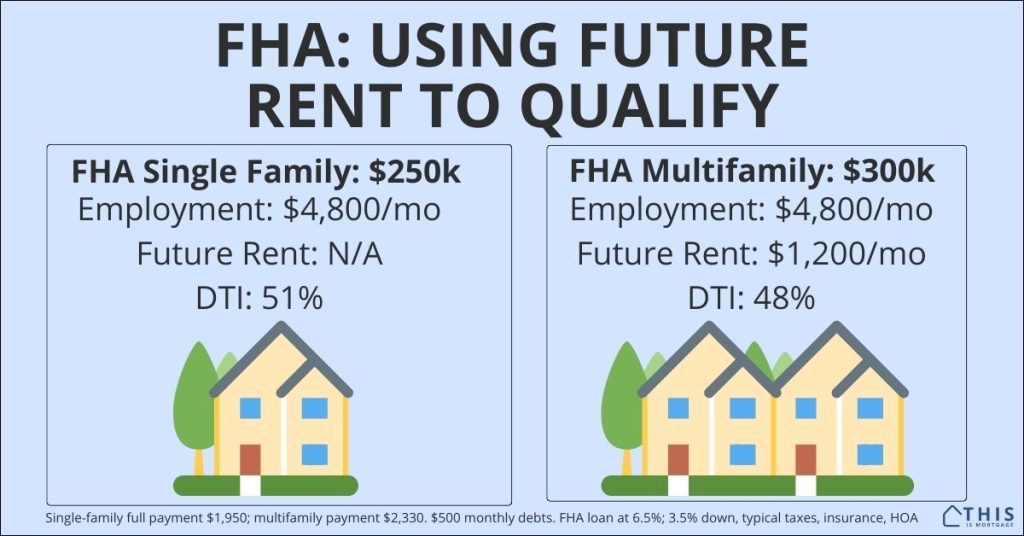

First things first, the property must be a 2-, 3-, or 4-unit multifamily property. FHA does not allow you to use rental income on a single-family home unless there’s an accessory dwelling unit on the property.

You must also live in one of the units as your primary residence.

The lender will use a rent calculation and add it to your employment income. You can then use a combination of employment plus rent to qualify.

Here’s how that could help you qualify.

| FHA 1-unit | FHA 2-unit | |

| Home price | $250,000 | $300,000 |

| Full payment* | $2,200 | $2,500 |

| Other debt payments | $500 | $500 |

| Employment income | $5,200 | $5,200 |

| Net rental income | n/a | $1,200 |

| Qualifying income | $4,800 | $6,400 |

| DTI | 52% | 47% |

| Result | May not qualify | May qualify |

*Assumes FHA loan at 7.5%, 3.5% down, FHA MIP, typical taxes, insurance, HOA.

There are many instances where you may be approved to buy a 2-4 unit property more easily than a single-family home.

Find a lender to check your multifamily eligibility.

How do you prove future income?

Proving future income on an FHA multifamily home is not as hard as it sounds. Assuming you have no history of collecting rent from this property, here’s what you need.

- If units are currently rented: Supply the lender with current lease agreements for all units that you won’t be occupying.

- If units are not rented: The FHA appraiser will complete a few different reports including an income/expense analysis (Fannie Mae 216/Freddie Mac 998) and a market rent analysis (Fannie Mae 1025/Freddie Mac 72).

From there, the lender will use the lesser of:

- The projected income based on an income/expense estimate

- 75% of fair market rents or actual rents, whichever is lower

For example:

| Report | Rent amount | Net rent |

| Income/expense analysis | $800/mo | $800/mo (no deduction required) |

| Market rent analysis | $1,100/mo | $825 (75%) |

| Current lease | $900/mo | $675 (75%) |

| Rental income used | $675 |

In the above example, the income/expense method does not need to be reduced because it already factors in a vacancy rate.

The other two methods require a 25% reduction since FHA assumes the property will be vacant 25% of the time, even though that’s very conservative. True vacancy rates in good markets are more like 5-10%.

Maximizing future qualifying rental income

Take a look at the example above. You’ll note that you have to use 75% of current rents to qualify, even though the unit could rent for more.

This is likely because HUD, the overseer of FHA, assumes you will not or can not charge higher rent or evict current tenants to raise rent.

So one strategy is to find a multifamily property without current tenants. These properties can be hard to find, though, so you may need to purchase a property with current leases in place.

Some properties have long-term tenants that are paying well below market rent. This is a sign of mismanagement. The landlord didn’t keep up with market rents.

Related: Buying A Fully Occupied Multifamily Home Using FHA

The tenants will never leave. One strategy (though it might sound heartless) is to declare that you will live in the unit with the lowest current rent. The tenant will have to move on. Then you can qualify (and make more money) from the higher-priced units.

This should be a business decision and you shouldn’t feel bad for displacing a low-paying tenant.

Get started on your FHA multifamily loan by contacting a lender.

More about the appraiser’s reports

The appraisal rent analysis can seem mysterious. What are these forms?

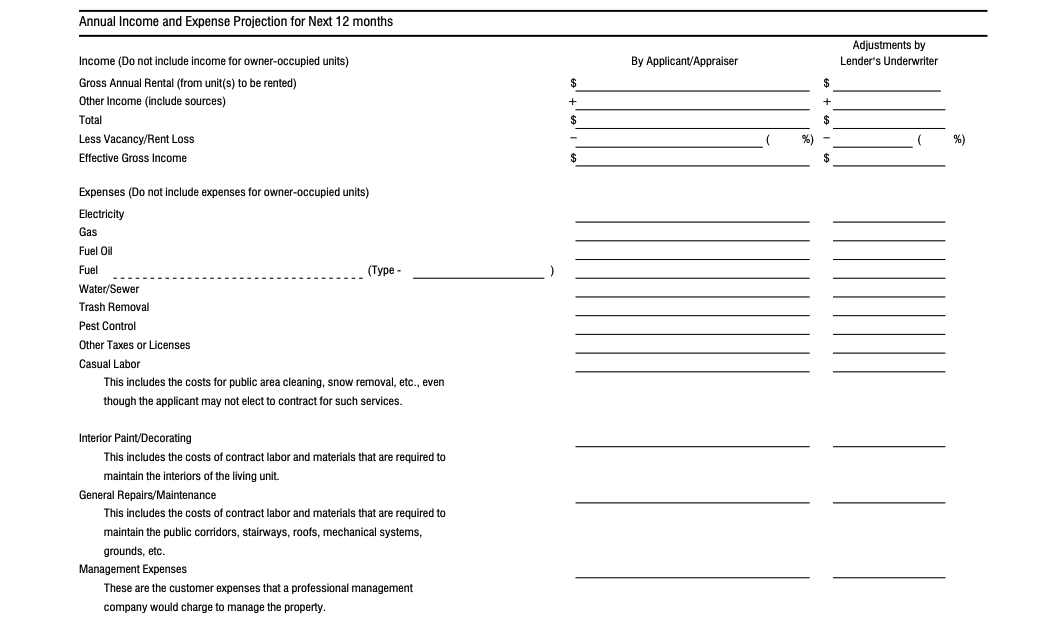

Operating Income Statement (Fannie Mae Form 216/Freddie Mac Form 998): If you’ve ever seen a “P&L” or profit and loss statement from a business, this form might be familiar. This is the appraiser’s version. It attempts to calculate income and expenses from each unit to arrive at a net cash flow. Here’s a small snapshot of this form which is a few pages long. If you’d like to see the whole thing, download it here.

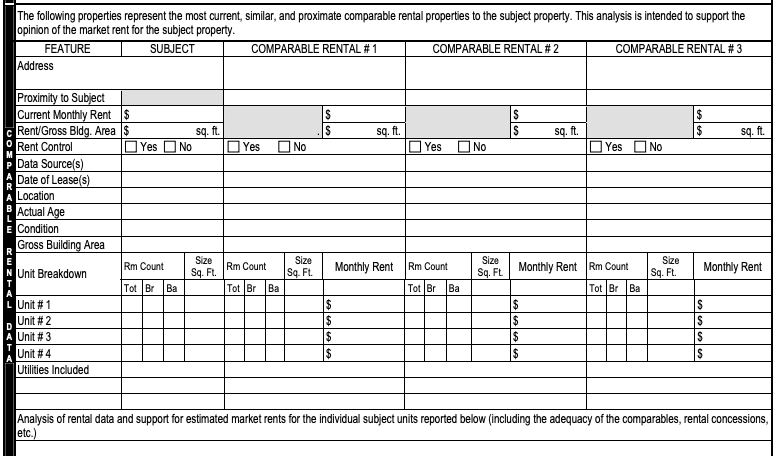

Small Residential Income Property Appraisal Report (Fannie Mae Form 1025/Freddie Mac Form 72): This is similar to the single-family appraisal report, except it is specific to 2-4 unit properties. It reviews comparable rentals in the area as well as comparable sales. Its purpose is to determine market rents for each unit as well as the value of the entire property. Below is an image of a part of the form, or you can download it here for a full view.

Rental income from another property

This is a very different topic, one that will be covered in a separate article. FHA rental income guidelines can get very muddy when trying to talk about two things at once: 1) the property you’re buying (the “subject property”) and, 2) a different property you own for which you collect rent.

To keep things clear, this article refers only to rental income on the subject property, the one you plan to buy.

A “gotcha”: the FHA self-sufficiency test

More is not always better when buying a multifamily home with FHA.

Recently, HUD started requiring the FHA self-sufficiency test for 3- and 4-unit properties. The rule doesn’t apply to duplexes.

The rule states that the property must bring in enough income to cover its full payment. Rates and prices are much higher than just a few years ago. It’s becoming increasingly difficult to get a property to pass the test.

Related: FHA Self-Sufficiency Test Calculator

You may want to keep things simple by looking for a duplex rather than a triplex or quad.

Run your scenario by a lender to check your multifamily eligibility.

My lender says I can’t use future rental income to qualify

Your lender may say you can’t use future rental income to qualify.

If this happens, shop around for a different lender.

This is an example of a “lender overlay” which is when a lender imposes additional rules on top of FHA guidelines.

You should have no trouble finding a lender that will underwrite “by the book” without extra rules. To be connected to one, start here.

Further considerations

Remember that owning a home is a big responsibility and becoming a landlord at the same time is much bigger.

Sure, you have to fix things when they break, which requires some financial reserves.

But a landlord has to deal with “people issues” which can be even more difficult.

What if your tenant can’t pay rent because their mom passed away? Do you let it slide? At what point do you re-establish rules? These situations will come up, guaranteed. And they are made harder because your tenant shares a wall with you.

Keep in mind, though, that nothing worth doing was ever easy. Rather, lofty goals are full of learning, gray area, and tough decisions.

This is the real world of landlording. It’s not relaxing on the beach like you see on Instagram. Believe me, I have two rentals.

As long as you go into it with realistic expectations, treating it like a business and not a cash cow or get-rich scheme, you’ll do alright.

Speak to a lender to see if you can become a multifamily homeowner.

FHA rental income guidelines FAQ

No. FHA guidelines state that you may count future rents toward income even without landlord experience. If your lender tells you otherwise, they are imposing additional rules on top of FHA guidelines, called overlays.

No. The rental income alone will not be enough to qualify you for the property. Employment income will be the majority of qualification income. Rental income is only a supplement.

Yes. Buying a multifamily home and living in one unit is known as “house hacking”. The strategy is to live in the property 12 months (the minimum requirement), then convert the entire property into a rental. This method is simply a way to get into a rental property or future rental property with a small down payment.

How to apply

Applying for an FHA multifamily loan is just like applying for any other home purchase.

Contact a lender and supply income, asset, and credit information, along with the type of property you’d like to buy.

The lender will work up a maximum home price and issue you a pre-approval you can use to shop for homes.

Once you find a home, the lender will work with you to close the home purchase.

Start here to apply with a lender.

Buying an FHA multifamily: A worthwhile goal

For those who can handle it, buying a multifamily property with a 3.5%-down FHA loan is a great idea. It launches you into real estate like few other things.

And that you can use future rental income to qualify is icing on the cake.

Speak to a lender now about multifamily home loans.