For most FHA loans, mortgage insurance costs 0.55% of the loan amount annually and 1.75% of the loan upfront.

- FHA monthly mortgage insurance: 0.55% of the loan per year paid in 12 installments

- FHA upfront mortgage insurance: 1.75% of the loan amount financed at closing

For example, a $250,000 home would require $112 per month and a one-time financed mortgage insurance fee of $4,222, assuming a 30-year, 3.5% down FHA loan.

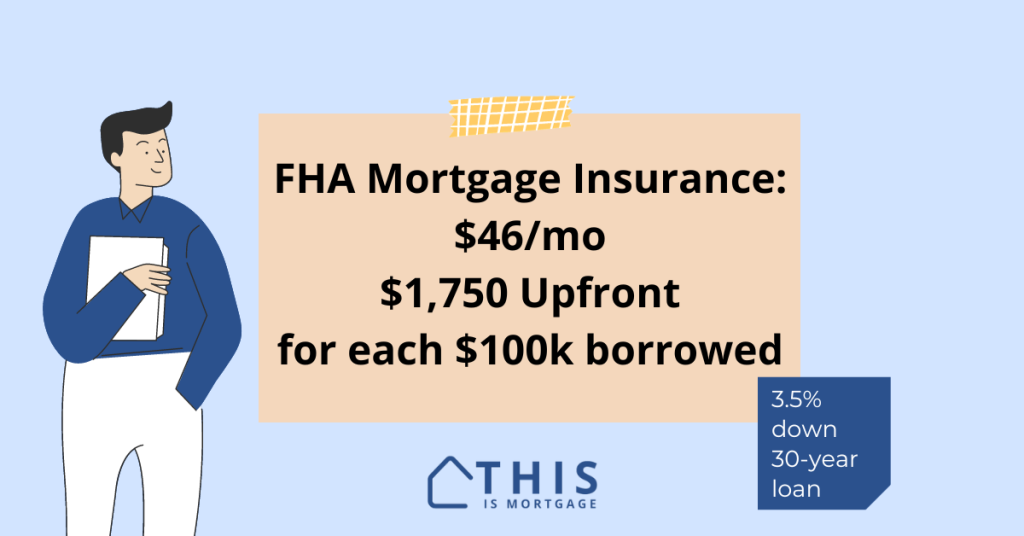

Another way to think about it is $1,750 upfront and $46 per month for each $100,000 borrowed.

Check your eligibility to buy using FHA.

Here’s what you will pay for upfront and monthly mortgage insurance premiums, also called MIP, based on your home price.

| Home Price | Monthly MIP* | Upfront MIP* |

|---|---|---|

| $75,000 | $34 | $1,267 |

| $100,000 | $45 | $1,689 |

| $150,000 | $68 | $2,533 |

| $200,000 | $90 | $3,378 |

| $250,000 | $113 | $4,222 |

| $300,000 | $135 | $5,066 |

| $350,000 | $158 | $5,911 |

| $400,000 | $180 | $6,755 |

| $450,000 | $203 | $7,599 |

| $500,000 | $225 | $8,444 |

*Assumes 3.5% down, 30-year loan

Your FHA MIP may vary depending on loan amount, down payment, and loan term. But the vast majority of FHA borrowers will pay the above amounts.

See how much home you can afford using an FHA loan.

FHA MIP levels for all loans

| Loan Amount | Down Payment | Annual Cost (pay 1/12 per month) |

|---|---|---|

| 30-year loans | ||

| <$726,200 | Less than 5% | 0.55% of loan |

| <$726,200 | More than 5% | 0.50% of loan |

| >$726,200 | Less than 5% | 0.75% of loan |

| >$726,200 | More than 5% | 0.70% of loan |

| 15-year loans | ||

| <$726,200 | Less than 10% | 0.40% of loan |

| <$726,200 | More than 10% | 0.15% of loan |

| >$726,200 | Less than 10% | 0.65% of loan |

| >$726,200 | 10-22% | 0.40% of loan |

| >$726,200 | More than 22% | 0.15% of loan |

How do you pay for FHA MIP?

Though FHA MIP is referred to as “annual,” you will pay it monthly. Your lender will split it up into 1/12 installments.

You won’t make a separate payment. The lender lumps the mortgage payment, mortgage insurance, property taxes, and insurance into one monthly bill. This ensures on-time payment of all these costs.

You pay the upfront portion of MIP at closing. Most borrowers choose to wrap this cost into the loan amount. This increases your payment slightly but lowers the amount of cash needed to close the loan.

Is FHA mortgage insurance permanent?

FHA mortgage insurance is permanent unless you put 10% down. Most borrowers will pay FHA mortgage insurance for the life of the loan since most put down 3.5%.

But many people carry the FHA loan only a few years, then refinance into a conventional loan. With 20% or more equity, the new conventional loan does not require PMI.

Those who put 10% down or more will pay MIP for 11 years.

There is some interest in ending permanent FHA mortgage insurance from the government.

FHA mortgage insurance reduction introduced in 2023

In February 2023, FHA mortgage insurance was reduced by 0.30% of the loan per year from 0.85% to 0.55% for most FHA loans. The savings are significant.

Someone purchasing a $250,000 home saves about $60 per month compared to pre-2023 FHA buyer, an important discount as rates hit multi-decade highs in 2023.

As of now, there is no expiration to this reduction in 2024.

See if you qualify for an FHA loan.

Mortgage insurance for FHA refinances

All borrowers receiving an FHA Streamline refinance will pay 0.55% of the loan per year. An FHA Streamline is an easy way to reduce your rate with no appraisal or income documentation required.

You may be eligible for an upfront mortgage insurance refund. You must refinance into another FHA loan, such as the FHA Streamline, within three years.

FHA offers this discount to remove some of the cost of getting into a lower rate if they fall, as they are expected to in 2024.

Is FHA MIP worth it?

One of the biggest issues homebuyers have with FHA is its mortgage insurance. Mainly, that it is permanent.

However, most buyers should not make this a deal breaker. Many buyers have the FHA loan only a few years then refinance into conventional when their credit improves or they have more home equity.

FHA’s primary purpose is to get people into homes and it does that well. Most people don’t keep the loan forever, though.

As a way to break into the housing market, FHA is hard to beat. In fact, its mortgage insurance is cheaper than conventional PMI for most buyers.

Unless you have excellent credit, you will likely pay 2-3 times as much for conventional mortgage insurance.

FHA MIP is 0.55% per year while conventional PMI ranges from about 0.40% to 1.90% for similar down payments, according to MGIC.

Mortgage insurance is never fun to pay, but you’ll probably pay a lot less of it using an FHA loan unless you have a large down payment and great credit.

FHA MIP alternatives

If you use an FHA loan, mortgage insurance is always required.

You may avoid PMI on a conventional loan if your credit and loan profile are strong enough.

For instance, some conventional lenders allow lender-paid PMI option. With these loans, the lender issues a higher mortgage rate in lieu of requiring monthly PMI. These aren’t always the best deal, though, since you can’t cancel PMI later (you keep paying it in the form of a higher rate).

You can also try a piggyback loan if you have 10% down. This is where you finance half of your 20% down payment with a second mortgage.

You can also avoid mortgage insurance altogether by coming up with 20% down and using a conventional loan. However, this level of down payment is typically unattainable for first-time buyers.

FHA mortgage insurance: a better deal than you think

FHA mortgage insurance offers great value for the money. You can own a home without perfect credit and just 3.5% down. And even this money can come from gift funds or down payment assistance.

Monthly mortgage insurance is a small price to pay for this opportunity.

Take advantage of today’s low FHA mortgage insurance rates and see if you qualify to buy a home.

Check your eligibility for FHA.