If I Make $200,000 A Year What Mortgage Can I Afford?

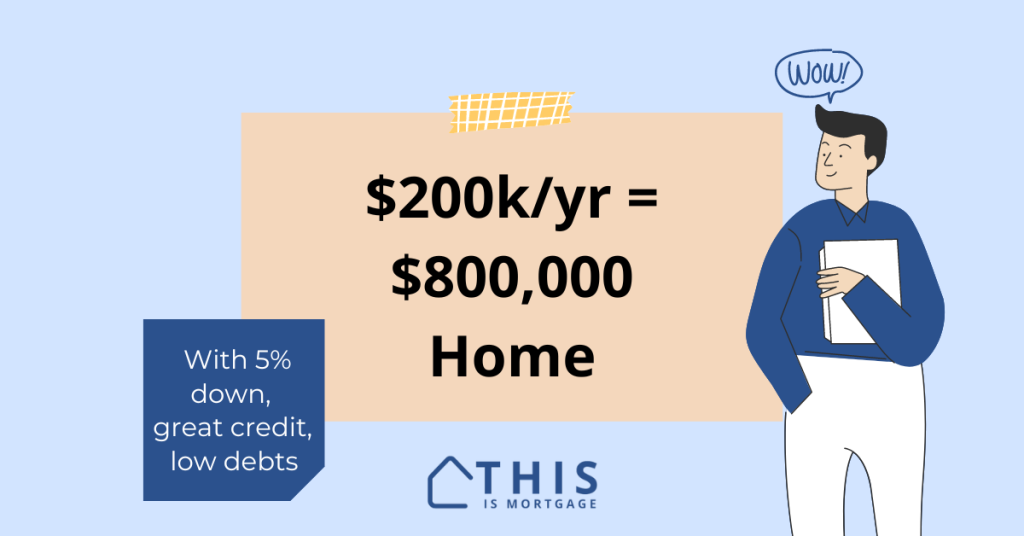

You can afford a home up to $800,000 with a mortgage of $760,000.

This assumes a 5% down conventional loan, low debts, good credit, and a rate of 7%, and a total debt-to-income ratio of 45%.

Keep in mind that many factors can influence this number like property taxes, homeowner’s insurance, HOA dues, credit score, and more. Apply with a lender to find your personalized maximum home price.

Speak to our lending team to see what you can afford with a $200k salary.

Home affordability by monthly debt payments

Your debt level affects your buying power perhaps more than anything else.

For instance, say you have $1,500 in monthly debt payments like student loans and credit card payments. At a salary of $200,000 per year, adding a $750-per-month auto payment would reduce your maximum home price by $110,000.

Related: The Average Car Payment Reduces Home Buying Power By $110,000

Lenders can approve you for a payment up to about 45% of your gross monthly income toward debt payments. That’s roughly $7,500 for an annual salary of $200,000. About 36% of your gross income ($6,000) can be used for the house payment leaving about 9% of income for other debts.

| Yearly income | $200,000 |

| Monthly income | $16,667 |

| Max house payment (36%) | $6,000 |

| Max total debt + housing payments (45%) | $7,500 |

In mortgage-speak, that’s a 36% front-end debt-to-income (DTI) ratio and a 45% back-end DTI. This is about the highest DTI lenders will approve at this loan amount.

Following is what you might qualify for depending on your current debt load.

| Annual Income | Monthly Debt | Max House Payment | Home Price |

|---|---|---|---|

| $200,000 | $0-$1,500 | $6,000 | $800,000 |

| $200,000 | $2,000 | $5,500 | $725,000 |

| $200,000 | $2,500 | $5,000 | $650,000 |

| $200,000 | $3,000 | $4,500 | $580,000 |

| $200,000 | $3,500 | $4,000 | $500,000 |

*Assumes a conventional loan at 5% down and 7% interest rate, $500/mo property taxes and $100/mo insurance, 740 credit, 0.53% mortgage insurance factor, no HOA. Your rate and costs will vary.

Related: Buying a Home With Zero Down Payment

Connect with a lender to see what you can afford.

Maximum home price by down payment

Your down payment dramatically affects affordability.

For one, your loan balance drops with a higher down payment, resulting in a lower payment. Additionally, you pay less mortgage insurance or none at all when you put more down.

| Annual Income | Down Payment | Monthly Payment | Home Price |

|---|---|---|---|

| $200,000 | 5%* | $6,000 | $800,000 |

| $200,000 | 10% | $6,000 | $860,000 |

| $200,000 | 20% | $6,000 | $1,010,000 |

*Note that a 3.5% down FHA loan is not available in most areas, since the FHA loan limit in most of the U.S. is $472,030 for 2023. Likewise, a 3% down conventional loan is not available for loans more than the standard conventional limit of $726,200. Calculations assume a conventional loan with 5-20% down, 7% interest rate, $500/mo property taxes and $100/mo insurance, standard mortgage insurance, 740 credit score, no HOA. Your rate and costs will vary.

No down payment? Speak to a lender now about down payment assistance programs.

Maximum home price by interest rate

Interest rate is another significant determiner of your maximum home price. If rates drop, it’s a great time to enter your home search.

| Annual Income | Interest Rate | Monthly Payment | Home Price |

|---|---|---|---|

| $200,000 | 8% | $6,000 | $730,000 |

| $200,000 | 7% | $6,000 | $800,000 |

| $200,000 | 6% | $6,000 | $875,000 |

| $200,000 | 5% | $6,000 | $975,000 |

*Assumes a conventional loan at 5% down, up to $1,500/mo debt payments, $500/mo property taxes and $100/mo insurance, 740 credit, standard mortgage insurance, no HOA, 45% backend DTI. Your rate and costs will vary.

Maximum home price by desired debt-to-income level

While many financial gurus suggest you should have a debt-to-income of 25% or less, it’s just not realistic in most markets. Pushing your total DTI from 25% to 45% increases your buying power by $275,000 at an income of $200,000.

| Annual Income | DTI | Payment | Home Price |

|---|---|---|---|

| $200,000 | 25% | $4,167 | $525,000 |

| $200,000 | 35% | $5,833 | $780,000 |

| $200,000 | 45% | $6,000 | $800,000 |

*Assumes a conventional loan at 5% down, 7% rate, no debts for 25% and 35% scenarios, $500/mo property taxes and $100/mo insurance, 740 credit, standard mortgage insurance, no HOA. Your rate and costs will vary.

Ways to increase your buying power

If you’re struggling to find a home that you can qualify for, there are ways to increase your maximum purchase price.

Consider an adjustable-rate mortgage (ARM): As seen above, reducing your rate from 7% to 6% can increase your buying power by $75,000 at your income level. An ARM rate eventually adjusts but starts off fixed for at least 3-5 years. That’s a lot of time to refinance or increase your income to afford a potentially higher payment later.

Buy down your rate: Consider buying down your rate with points, especially if you can get closing cost credit from the seller or builder.

Avoid HOAs: Homeowner association dues can be hundreds of dollars per month. Dues add to your DTI which limits your buying power.

Make a bigger down payment or get gift funds. The lower your mortgage balance, the lower your payment will be. Try to find a down payment assistance program or get a gift from family to reduce your loan amount.

Use an FHA loan. While the maximum loan is only about $472,000 in most areas, these loans are lenient on debt-to-income ratios. Conventional loans limit you to about 45% DTI including all debts and housing payment (50% in select cases). FHA’s max is 46.9% front-end DTI and 56.9% back-end.

Pay off debt: Paying off a $750 car payment can increase your buying power by $110,000.

Request a call from a lender to see what you can afford with a $200k salary.

FAQ

Depending on your existing debts, you may be able to afford an $800,000 home with 5% down ($760,000 mortgage). Your exact price depends on your debts, interest rate, property taxes, homeowner’s insurance, HOA dues, loan program, and payment comfort level.

Reducing your debt payments by $750 per month can increase your maximum home price by about $100,000 if you make $200,000 per year. Paying off debt will help you qualify for a better home that will suit your needs longer.

You don’t need a high credit score, but it will help you qualify for more. Conventional mortgage insurance is expensive for those with credit scores below about 720.

You can afford a lot of house with a $200k salary

If you have a good salary and credit, you might be surprised at what you can afford. Get started on your pre-approval so you’re ready when you find the right home.

Speak to a lending professional to see if you are eligible to buy a home.