Buying a foreclosed home sounds great. They are offered at bargain-basement prices and you can achieve fast equity by fixing it up.

And buying a foreclosure with a USDA loan would be even sweeter: get a zero-down loan AND a low home price? Yes, please.

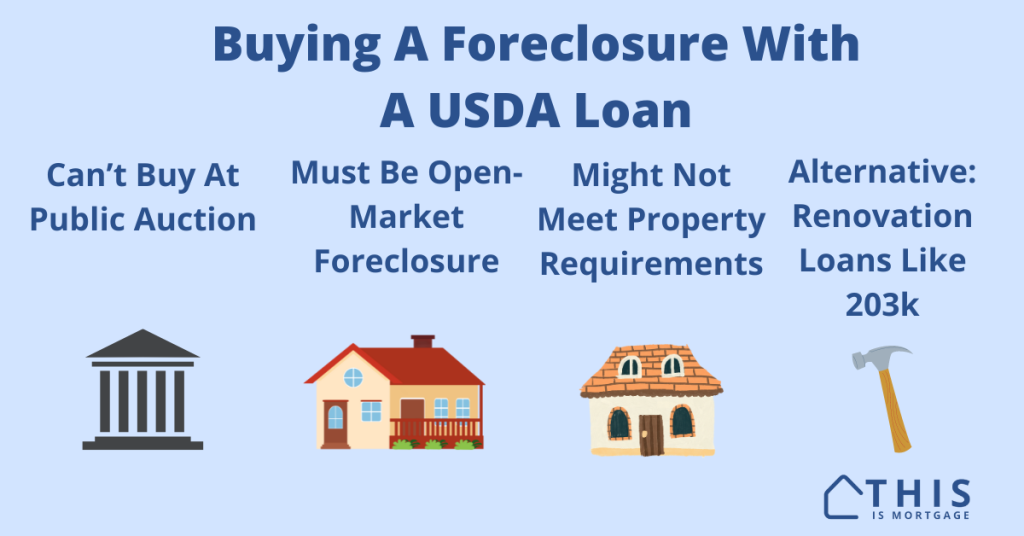

So, can you buy a foreclosure with a USDA loan? Technically, yes, if it’s within a USDA-eligible area, your income does not exceed program limits, and you qualify for the loan.

However, a lot depends on where in the foreclosure process the home is:

1. At public auction (trustee’s sale)

2. On the open market

Let’s see if USDA will work in these cases.

Connect with a USDA lender to see if you can buy a foreclosure.

Buying with USDA at public auction (trustee’s sale)

A public auction is the bank’s first attempt to sell the home after it’s foreclosed on. Often, these sales occur on the courthouse steps, literally, as “wild west” as that sounds.

You likely can’t buy a foreclosure at this stage with any financing. These homes are snatched up by experienced investors with cold, hard cash.

This is because cash sales close the same day, without an inspection, appraisal, or extra lender requirements. It’s unlikely that the bank seller will wait around for a mortgage to close at this point.

In fact, USDA has its own foreclosed properties, and it doesn’t even accept USDA financing for them. Check or cash only. That should tell you something.

Buying an open-market foreclosure listing with USDA

Realtor.com’s foreclosure database and similar sites show open-market foreclosed properties.

Wait a minute, you say, I thought foreclosures were sold on the courthouse steps.

They are, but if it doesn’t sell, the home is sent to an agent or company to sell like any other house. This is where it gets in front of more people, because not everyone can be on the courthouse steps at 8:30 AM on a Tuesday, for example.

At this stage, it’s much more feasible to use a USDA loan to purchase the property. You can make an offer with a USDA loan. There’s a chance the seller’s agent will accept. Then, at least in theory, you could close the loan.

But, there’s one more issue to deal with: The property’s condition.

USDA uses the same property standards as FHA

FHA loans are known for being pretty picky about the property condition. And guess which property standards USDA follows? Yep, those of FHA.

No handrail? Chipping paint? You have to fix it prior to closing.

The reason foreclosures are often cheaper than other homes is that they are in bad shape. Often, the former owner ran into financial trouble long before they were foreclosed on. They didn’t keep up on maintenance.

And, once the owners realize they will lose the home, it’s a free-for-all. They sometimes even rip out the appliances and sell them for extra cash before they’re evicted. This is the sad reality of foreclosures.

Most of these homes are sold as-is. That means the seller will do no repairs. The lender won’t approve it if it doesn’t meet USDA financing property requirements.

If you find a foreclosed property in great condition, you might just be able to buy with USDA, but the chances of finding such a property are slim.

Get pre-approved with a USDA lender so you’re ready to buy.

Can you buy a house with a hard money loan, then refinance with USDA?

Whether you’re buying on the courthouse steps or on the open market, you might have this question: Can you purchase with a hard-money loan, then refinance into USDA?

Unfortunately, you can’t refinance out of another loan type into a USDA loan. You have to have a USDA loan currently to refinance into another USDA.

However, here are some ideas:

1. Use a standard cash-out refinance to pay off the hard-money loan. If there’s enough equity in the home after repairs, you could use a conventional cash-out refinance up to 80% of the home’s new appraised value. There’s a 12 month waiting period after you purchase to obtain a cash-out loan. If you are not seeking cash-out, you could potentially get a standard rate-and-term refinance after repairs.

2. Get an FHA 203k loan which covers the purchase price and repairs. The home does not have to meet typical FHA property guidelines assuming any issues will be resolved with the repair work.

3. Apply for a Fannie Mae HomeStyle Renovation or Freddie Mac Choice Renovation mortgage. Like FHA 203k, you can finance the home purchase and bring the property up to an acceptable condition with one loan.

FAQ

USDA allows you to buy a foreclosed home if it meets minimum property requirements. USDA uses the same property condition requirements as FHA.

First, the home has to be listed on the open market. You can’t buy a foreclosure on the courthouse steps using USDA financing. Once it hits the open market, it has to be in good enough condition to qualify for a USDA loan. Most foreclosures are sold “as-is”, meaning the seller will do no repairs.

Try for an FHA 203k, Fannie Mae HomeStyle, or Freddie Mac ChoiceRenovation, all of which allow you to finance repairs into the purchase loan. Otherwise, use a hard money loan to purchase the property and attempt to refinance into a standard conventional loan when the home is repaired.

Buying a foreclosure with a USDA loan: a long shot, but possible

It’s worth at least trying to get an open-market foreclosure with a USDA loan. Just check the home’s condition if possible. Make sure you add a financing contingency into your offer so you can back out if the home doesn’t meet requirements.

With some luck, you could get a very affordable home with zero down.

Begin your USDA loan by finding your lender here.