What are $100 down HUD homes?

The Department of Housing and Urban Development, better known as HUD, offers its foreclosed homes for just $100 down.

Why? When someone gets an FHA loan, but doesn’t make the payment, HUD must foreclose on the property.

HUD does not want to hold onto these homes. HUD’s top goal is to offload its real estate portfolio to those who will live in the properties. One of the agency’s core missions is to enable affordable homeownership in the U.S., and this program aligns with the mission perfectly.

So how do you find a $100 down HUD home?

Set up a call with us to see if you are eligible for $100 down.

Finding $100 down HUD homes

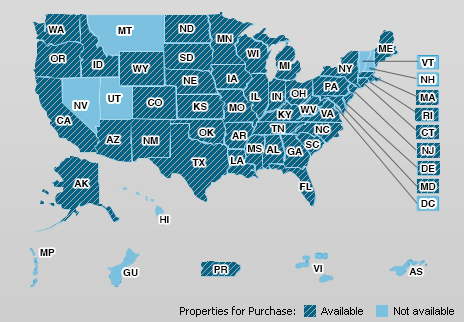

Available homes are easy to find on the HUD Home Store.

You will see a map like the one below. Shaded states have available homes.

Keep in mind that there may not be many homes available near you. Foreclosures of any kind are hard to find currently, due to a strong economy and strong homebuyer demand. People who can’t pay their mortgages simply sell on the open market.

Some buyers watch HUD’s website daily for new listings. When one appears, their agent makes an offer immediately.

Another reason to act quickly: There’s an initial 7-day period in which only owner-occupant offers are accepted. After that, investors and cash buyers can swoop in to grab these deals.

Homebuyers who are patient, but can act quickly, will eventually find a home to submit an offer on.

How to make an offer on a HUD home

Making an offer on a HUD home is a little different than with standard properties you see on the open market.

If you’re serious about purchasing one of these homes, your first step is to find a HUD-approved real estate agent. Only HUD-approved agents can submit offers. You can search for an agent in your area on HUD’s site, or your current agent can become HUD-approved.

Next, here’s what to do.

- Get a pre-approval from an FHA lender that offers the $100 down program

- Watch for homes that are within your price range.

- When one appears, examine its condition. Make sure you are okay with doing work yourself or financing repairs.

- Have your HUD-approved agent submit a full-price offer.

- Wait to see if HUD accepts your offer.

- If your offer is accepted, submit your earnest money, typically 1% of the home’s price up to $2,000.

Set up a call with a loan professional to see if you are eligible for $100 down.

Who qualifies for the $100 down program?

In short, anyone who qualifies for a standard FHA loan can qualify for the $100 down program, with a few additional rules.

- You must plan to live in the property

- 580 minimum credit score

- Must have sufficient funds to cover $100 down plus closing costs (typically 2-5% of the home’s price, but HUD covers up to 3%)

- Can document income and employment

- You have not owned a HUD home in the past 2 years

- No bankruptcies or foreclosures in the past 2 years

- Meet other FHA requirements

FHA is one of the easiest mortgage types to qualify for. Even if you don’t think you could ever own a home, the $100 down program could make you a homeowner.

Become a homeowner with the $100 down program. Request a call from our lending team.

How to buy a $100 HUD home that needs work

Just like any foreclosure, HUD homes may be in disrepair. One important aspect of making an offer is to make sure you are okay with doing some work yourself after closing.

However, some properties are not financeable with FHA as-is due to their condition. You can finance repairs into the loan using the FHA 203k loan.

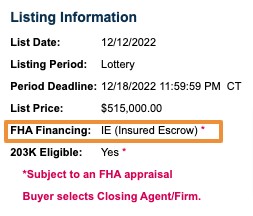

On the listing, you will see one of three codes:

- IN – Insurable by FHA (meaning you can get an FHA loan on it). No repairs needed.

- IE – Insured with Escrow. Repairs under $5,000 needed which can be financed using the FHA Repair Escrow program

- UI – Uninsurable. This means you need an FHA 203k loan to bring the home up to FHA standards

If the home requires financed repairs, make sure the home price plus repair budget is within your pre-approved loan amount.

How much money do I need for the $100 down program?

Though the program requires just $100 down, there are additional closing costs. However, HUD contributes up to 3% of the home’s price to help the buyer. Here’s an estimate of costs compared to the standard FHA program.

| $100 Down Program | Standard FHA | |

| Home price | $290,000 | $300,000 |

| Repairs financed | $10,000 | $0 |

| Down payment | $100 | $10,500 |

| Closing costs | $9,500 | $9,500 |

| HUD contribution | -$8,700 | -$0 |

| Cash to close | $900 | $20,000 |

In this example, the $100 down home requires $900 to close. But if this person purchased an open-market home with an FHA loan, their cash to close would be closer to $20,000.

$100 Down FAQ

You will need $100 for the down payment, plus closing costs. HUD covers up to 3% of the home’s price in closing costs, so you will need the rest, typically 1-2%.

There is no catch. HUD wants to offload its foreclosed properties to owner-occupants. So it offers these homes for $100 down and covers up to 3% of the home’s price in closing costs. The only “catch” is that there are currently not many homes available, so buyers who want to use this program must be patient and watch for new listings daily.

HUD often offers these homes at below-market prices. This discount combined with just a $100 down payment requirement eliminates many barriers for first-time homebuyers.

The $100 down program could make you a homeowner

There are not many programs on the market today that offer zero down or close to it. But thanks to HUD’s goal to offload its properties, many people are becoming homeowners with very little out of pocket.

See if you qualify for the $100 down program.

Request a call to review your $100 down eligibility.