The down payment requirement for a loan program often means the difference between qualifying or not.

Programs with the lowest down payments are often the most attractive. And when you’re buying a multifamily property, where loan amounts are much bigger, the lower the percentage down payment required, the better.

Here’s what down payment you can expect to pay for a multifamily property.

See if you qualify for a multifamily home loan.

- Multifamily down payment requirements by program

- Down payment example

- About down payments

- Why do most people choose FHA to finance multifamily?

- Where can down payment funds come from?

- What are ineligible sources of down payment?

- Why do lenders require a down payment?

- Multifamily down payment FAQ

- Multifamily down payments: bottom line

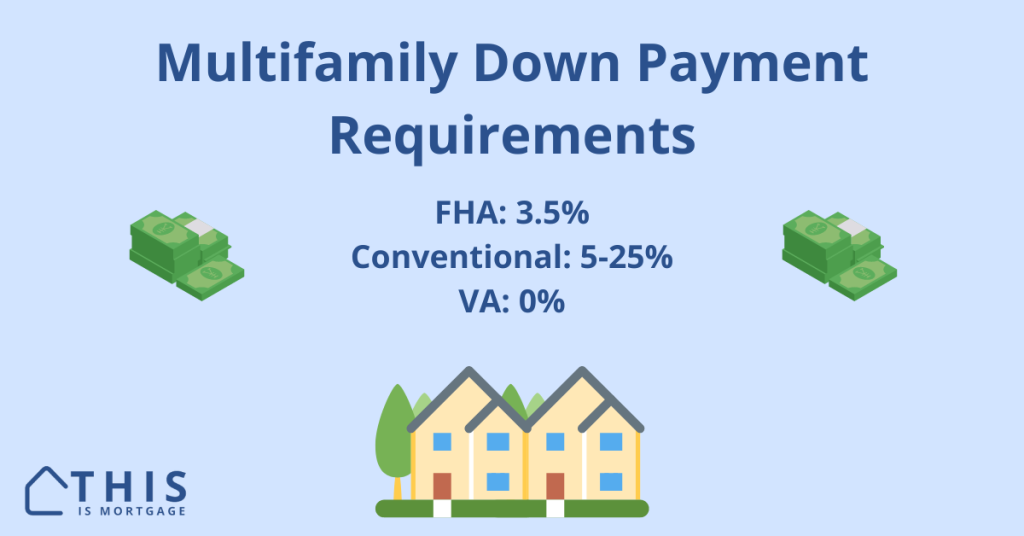

Multifamily down payment requirements by program

Here are down payment requirements for owner-occupied multifamily properties, meaning you will live in one unit.

- FHA multifamily down payment: 3.5%

- Conventional multifamily down payment: 5-25%

- USDA: N/A – single-family homes only

- VA multifamily down payment: 0%

| Loan Type | 1 Unit | 2 Units | 3 Units | 4 Units |

| FHA down payment | 3.5% | 3.5% | 3.5% | 3.5% |

| Conventional down payment | 3% | 5-15%* | 5-25%* | 5-25%* |

| USDA down payment | 0% | n/a | n/a | n/a |

| VA down payment | 0% | 0% | 0% | 0% |

*While the conventional Freddie Mac Home One loan allows you to buy a 2-4 unit property with 5% down, it comes with strict income limits that will make most multifamily buyers ineligible for the program. Standard conventional loans require 15-25% down for multifamily.

Down payment example

| FHA Duplex | Conventional Duplex | VA Duplex | |

| Home price | $300,000 | $300,000 | $300,000 |

| Down payment % | 3.5% | 15% | 0% |

| Down payment $ | $10,500 | $45,000 | $0 |

About down payments

Down payments are expressed as percentages of the purchase price. For example, 5% down on a $200,000 home would be $10,000.

Common down payments are 3.5%, 5%, 10%, and 20%. It’s not always necessary or even a good idea to make a large down payment. It’s often better to keep cash in reserve for emergencies.

This is especially true for multifamily properties, where you have multiple systems like furnaces, hot water heaters, and appliances that can break. Additionally, you may be without a tenant for a time, so extra cash can help.

Why do most people choose FHA to finance multifamily?

FHA offers the lowest down payment option for multifamily properties besides the VA loan, which is only available to current and former U.S. military veterans. FHA loans are available to just about everyone.

FHA multifamily loans require just 3.5% down, for any property of 1-4 units.

Compare this with most conventional loans, which require 15-25% down for a 2-4 unit property.

Combine FHA’s low down payment requirement with its minimum credit score of 580 and other leniencies, it’s easy to see why it’s a favorite for first-time buyers, house hackers, and owner-occupying investors.

Start your FHA multifamily home purchase.

Where can down payment funds come from?

Eligible down payment sources vary slightly depending on the loan type, but in general, you can make a down payment from the following sources.

- Checking and savings accounts

- Cash deposited into a financial institution

- Cryptocurrency converted to USD if you show 60+ days history of ownership

- Liquidated stocks, bonds, and CDs

- 401k loans and withdrawals

- Proceeds from the sale of an asset with proper documentation

- Gift funds from relatives or other eligible sources

- Down payment assistance sources

To verify personal funds, you’ll give the lender at least two months of bank or account statements.

For gift funds, you’ll need a gift letter completed by the donor and proof that funds were transferred.

For down payment assistance, provide your lender with the assistance program representative’s contact details.

Related: Multifamily vs Single-Family Home Purchase Calculator

What are ineligible sources of down payment?

Down payments may not come from:

- Contributions from an interested party to the transaction such as the seller, Realtor, lender, and builder.

- Borrowed funds, unless from a HUD-approved non-profit providing a down payment assistance loan

- Theoretical assets, such as equity in a vehicle, unless you sell the asset and verify receipt of funds

Why do lenders require a down payment?

Down payments are one of the highest predictors of a successful loan, as proven through lending data. The theory is that, the more someone contributes to the house purchase, the less likely they are to walk away if things get tough.

Another purpose of the down payment is so the lender can sell the home again if the borrower doesn’t make the payment. Because lenders often have to sell a foreclosed home at a discount, a larger down payment protects them from losing money.

However, with programs like FHA, the lender has little risk despite a low down payment. HUD will reimburse the lender for losses. That’s why lenders will offer a 3.5% down loan, even on a multifamily property.

Multifamily down payment FAQ

You pay the down payment at the very end of the transaction, known as “closing”. You will wire or bring a cashier’s check to the escrow company when you sign final documents. You pay the down payment and closing costs with one wire or check.

In addition to the down payment, you are also responsible for closing costs. These are for third-party fees like appraisal, title insurance, and escrow closing services. You may also need cash reserves – extra funds remaining in personal accounts after paying the down payment and closing costs.

Typically you can’t borrow a down payment, like with a personal loan or credit card. One legitimate source of down payment financing, though, is through a government-sponsored down payment assistance program. A HUD-approved agency can issue a down payment loan. These usually come with low or no monthly payments until you sell or refinance the home.

The best way to build savings is to contribute to a fund monthly before spending money on other things. You could also cut expenses from your budget to save more.

Multifamily down payments: bottom line

Most multifamily home loans require a down payment, but FHA can reduce your upfront cash outlay significantly. And, you can get assistance making the down payment, too.

With some creativity and savings goals, you could be a multifamily property owner sooner than you think.

Check your multifamily home purchase eligibility.